THE Federal Government on Wednesday as part of its agenda to gradually diversify the Nigerian economyfrom oil dependence by uplifting other sectors in the country has approved $268 million in soft loans to support entrepreneurs and innovators.

Vice President Yemi Osinbajo said, “Nigeria approved disbursing $268 million in funding to support agricultural entrepreneurs and young technology innovators”.

The presidency in a statement disclosed that one tranche of the funding, worth 90 billion Naira ($248 million), will be dispensed by the central bank as “soft loans” for people building small-scale agricultural businesses.

Another $20 million will provide funding support young innovators in technology.

Recently, the National Bureau of Statistics’s (NBS) report on Micro, Small and Medium Enterprises (MSME) shows that 85 per cent of businesses could not have access to external financing within 2013 and 2017.

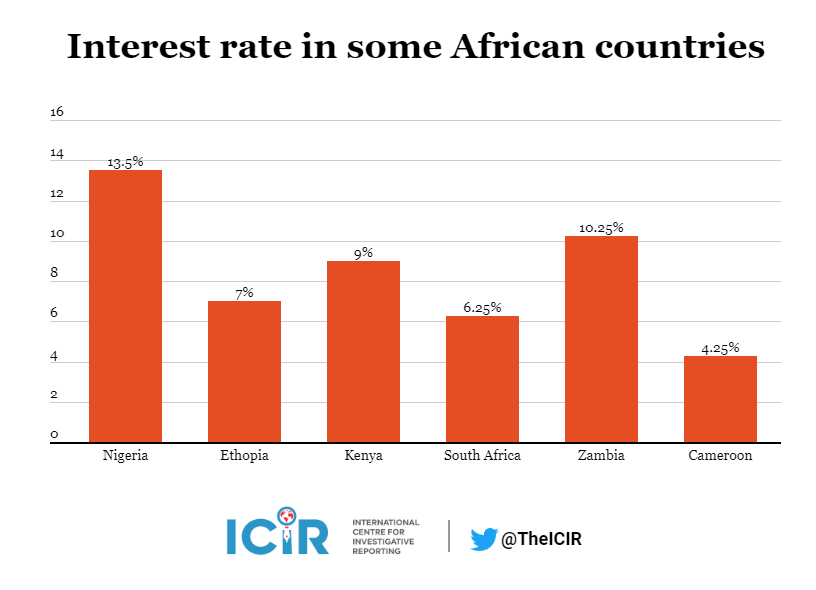

Nigeria’s benchmark interest rate is among the highest in Africa at 13.5 per cent. Ethiopia’s is 7 per cent; Kenya’s is 9 per cent; South Africa is 6.25 per cent; Zambia is 10.25 per cent, and Cameroon is 4.25 per cent.

A soft loan is a loan with no interest or a below-market rate of interest with lenient terms.

75% of the fund goes to agric startups? Other sectors need more support than this.