AS the Nigerian President Bola Ahmed Tinubu clocks 100 days in office today, September 5, some economic indicators already point to the impact of his reforms on the nation’s economy.

A former governor of Lagos State, Tinubu was sworn in as Nigeria’s president on May 29, 2023.

The Independent National Electoral Commission (INEC) had declared him the winner in the 2023 presidential election, but he still awaits the court’s final decision as two other opposition parties’ candidates are contesting the poll’s outcome.

During his inaugural speech, Tinubu highlighted some critical issues his administration set out to tackle.

“I had promised to reform the economy for the long-term good by fighting the major imbalances that had plagued our economy. Ending the subsidy and the preferential exchange rate system were key to this fight,” he said in a July national broadcast.

Tinubu pledged to double the annual economic growth rate to six per cent – or more.

Since assuming office, his major decision, which affects most citizens negatively by worsening existing hardship, is the fuel subsidy he suspended on the first day he assumed office.

Reforms too costly to bear

Notably, many experts have argued that the fuel subsidy removal and exchange rate unification are too costly to bear.

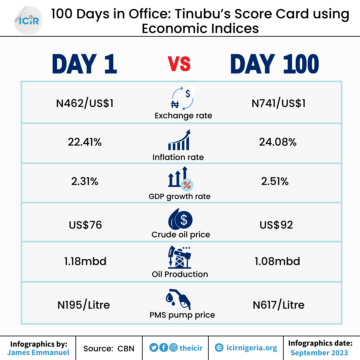

Fuel subsidy removal had seen the pump price of petrol jump by over 200 per cent from about N195 per litre to about N617 per litre.

The effects have been the rising transportation costs and snowballing prices of goods and services for households and businesses, among others.

Exchange rate unification has likewise impacted the sharp drop in the value of the naira against the dollar and other foreign currencies.

The exchange rate, around N462 to $1 when the new administration came in, has risen to N741 to $1. Inflation had risen from 22.41 per cent to 24.08 per cent.

“Our economy is going through a tough path, and you are being hurt. The cost of fuel has gone up. Food and other prices have followed it. Households and businesses struggle,” the President had admitted.

Hardship and more hardship…

Even though Tinubu’s initial steps enthused many people, it now elicited public backlash as food and transport costs surged.

In a July 31 address, the president acknowledged Nigerians’ hardship, heightened by his administration reforms.

He said the reforms are unavoidable, and he pleaded with Nigerians to be patient.

Following the ballooning suffering faced by the citizens, including civil servants, the Nigeria Labour Congress (NLC) embarked on a two-day warning strike on Tuesday, September 5.

The strike came after a similar action a month earlier.

In mid-July, the government declared a state of emergency, which allowed it to take exceptional steps to improve food security and supply, including clearing forests for farmland and improving access to seed and fertilisers.

As Nigerians await major harvests from the farms, hunger bites hard in most homes.

The humanitarian organisation Mercy Corps has reportedly illustrated how hard ordinary Nigerians have been hit by inflation, making it difficult for many to feed.

It found that food prices jumped by 36 per cent, and transportation fares rose by 78 per cent in the northern Borno state within a week after the government ended the fuel subsidy regime. It also revealed that hunger and incidents of petty theft grew.

“The sufferings are real and affect the citizens across all segments of our society – public service, private sector, informal sector, artisans, students, SMEs, the unemployed, the aged, pensioners, etc. There is, therefore, a need for urgent responsive actions from all tiers of government,” an economist, Muda Yusuf, told The ICIR.

He added that mitigating measures should be holistic, inclusive and driven by direct interventions, fiscal policy measures and monetary policy actions.

The federal government has provided soothing relief, known as palliative, to support vulnerable citizens, but few beneficiaries have received support aid.

Impact on businesses

Four critical sectors (oil refining, crude petroleum and gas, textile and livestock) of the economy had slid into recession in the year’s second quarter.

Yusuf said the sectors have been struggling because of macroeconomic, structural and policy issues.

The gross domestic product (GDP) fell by 2.5 per cent year-on-year in Q2 compared to 3.54 per cent in the same quarter last year.

An economic mix solution

Solving Nigeria’s economic challenges lies in addressing the issues around liquidity, stability, growth, and harmony, said a renowned economist and chief executive officer (CEO) of the Economic Associates (EA), Ayo Teriba.

Teriba had told The ICIR that the transition of power to President Tinubu offered Nigeria an excellent opportunity to make fresh efforts to solve its lingering economic problems and stabilise its economic growth and progress.

He had said the solution lay in the President taking a holistic, inclusive and sequential approach to four dimensions – liquidity, stability, growth and harmony.

“You cannot talk about stability without liquidity, you cannot talk about growth without stability, and you cannot talk about harmony without growth,” the economist explained.