ECONOMIC indicators are pointing to a challenging time for Nigerians in 2023. The President Muhammadu Buhari administration, left with barely six months in office, will have to take some hard decisions to address the inclement situation.

The economic headwinds are not unexpected to be compounded by rising inflation, overburdening taxes, expected food price surge, naira deprecation and weak economic growth.

Buckled by inflationary pressure, with the November inflation rate at 21.47 per cent, food prices are expected to surge this year with the country yet to recover from the destructive effects of floods that ravaged its food belt last year.

The World Bank has cut Nigeria’s 2023 economic growth projection to 2.9 per cent, from a previous projection of 3.1 per cent. This, the bank explained, was informed by production challenges in the oil sector, rising insecurity and flooding.

Also, a Fitch Solutions Country Risk and Industry Research report has predicted that the Nigerian economy would continue to slump in 2023 due to activities leading to the general election.

READ ALSO:

N100,000 weekly withdrawal limit will cripple businesses – NECA

Tinubu promises to protect Igbo businesses, make South-East Taiwan of Africa

Businesses lament as exchange rate problems erode capital

Twenty-three Nigerian businesses among 60 African startups to receive Google $4m grant

To fix up this concern, the government is targeting intense borrowing to fund its 2023 deficit budget, which has remained a problem to the economy. Analysts say that with the budget to be funded largely by borrowing, projected revenues and macroeconomic fundamentals, if not met, would put the country in huge economic distress.

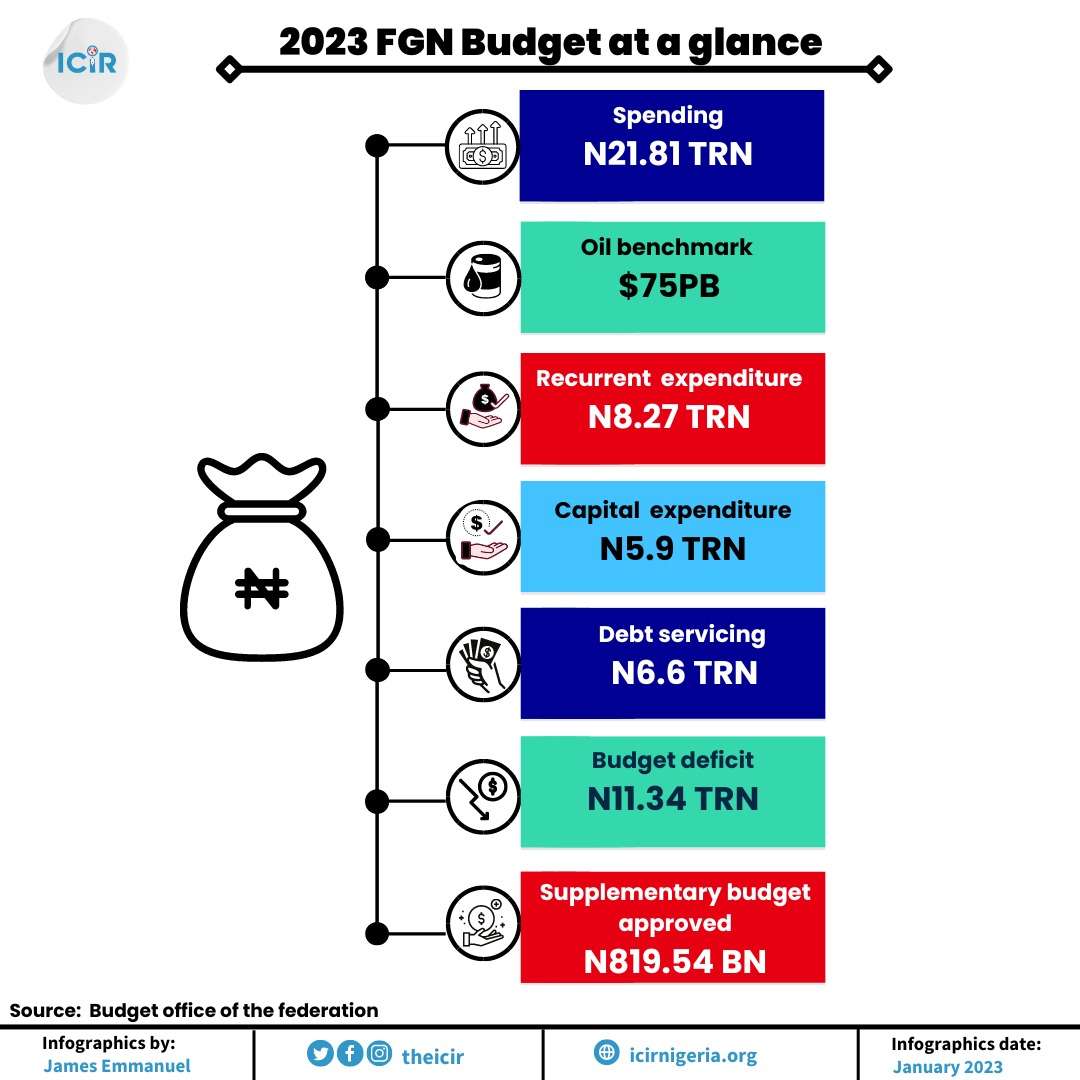

From the 2023 budget, the sum of N11.34 trillion is to be used to finance the budget deficit. The deficit figure is to be largely financed by N7 trillion of domestic debt, N1.76 trillion from foreign debt and N1.77 trillion from multilateral lending agencies like the World Bank and the African Development Bank. The sum of N206.1 billion will be sourced from privatisation proceeds.

The macroeconomic fundamentals in the budget also showed an oil production target of 1.69 million barrels per day, the official exchange rate pegged at N435.57/US$1 and inflation at 17.16 per cent. The macroeconomic fundamentals are subject to key global and economic factors like the Russia-Ukraine war, and crude theft in the Niger-Delta.

Budget analysts have allayed the fear that the Federal government would be leaning on heavier taxation to shore up its projected revenue.

Economic watchers say such a move would put the private sector into more uncertainties.

The Finance Bill passed by the National Assembly in December 2022 amended several laws, namely the capital gains, Tax Act, Companies Income Tax Act, Personal Income Tax Act, Petroleum Profit Tax Act, Stamp Duties Act, Value Added Tax, and Procurement Act.

There are concerns that businesses could be overburdened with taxes, which could see many in further distress, amid double-digit inflation of 21.47 per cent in November.

“This is a piece of legislation which has profound implications for investment, citizens’ welfare and the Nigerian economy. It is serious and puzzling that the Senate gave just 24 hours’ notice for stakeholders to attend a public hearing in December 2022.There is no better expression of deliberate exclusion from this important legislative process,” said the Executive Director for Centre for the Promotion of Private Enterprise, Muda Yusuf.

Besides the issue of increasing taxation, there is also a major factor of currency problems, spurred largely by naira deprecation and exchange rate volatility.

It is widely agreed government’s unregulated borrowing from the Central Bank to the tune of N23.7 trillion has wider implications on Nigeria’s currency, inflation, and even Nigeria’s quoted companies that have foreign debt exposure.

The World Bank has urged Nigeria to have a stable exchange rate, something the apex bank has not been able to achieve, with the wide gap in official and parallel markets causing problems for businesses and investments.

A research by the Economic Intelligence Unit (EIU) projected the 2023 Nigerian economic and political outlook as one of instability.

The EIU, like the World Bank, has revised down its real gross domestic product (GDP) growth estimate for 2023 to 2.8 per cent from 3.1 per cent, owing to tighter credit conditions, floods and widening insecurity.

On currency and lending problems, the intelligence outfit said hard currency remains in short supply, although the Central Bank of Nigeria (CBN) has reiterated its resolve to tame the parallel foreign exchange market.

“Inflation is expected to remain in double digits, and monetary conditions will be tight, with the central bank’s policy rate expected to peak at 17 per cent by end-2022 or early 2023, and to be maintained at this level throughout the year,” the EIU forecast.

Economic watchers agreed with the EIU’s position on inflation, saying Nigeria’s double-digit inflation figure has taken a deep cut at Nigerians’ earnings, plunging more people into economic difficulties.

“As at January this year, headline inflation was 15.60 per cent, and rose to a peak of 21.47 per cent in November 2022. Meanwhile, food inflation consistently outpaced headline inflation and core inflation during the year. For the basket of goods and services consumed by the average Nigerian, costs have accelerated by between 50 per cent and 100 per cent in 2022,” Yusuf said.

He said that the Buhari administration would need to address key drivers of inflation, boost productivity in the economy to drive output growth, stem the depreciation of the naira, and address the illiquidity in the foreign exchange market to soften the ground for his successor.

For a restaurant manager Oluchukwu Mgbemena, who does her trade in Abuja, high food prices are already taking their toll on her business.

Oluchukwu said, “I have noticed a sharp rise in prices this first week in the year that I went to the market. Rise in prices of stockfish, crayfish, dry fish and meat of assorted types is a major worry for us.”

She said she had had to readjust prices on her food menu to enable her to sustain the business.

2023 budget could worsen inflation with rise in borrowing

The government’s passage of the 2023 budget should ordinarily offer hope to many Nigerians. However, the realisation that a large chunk of the budget will be financed by massive borrowings is not offering optimism.

The N21.83 trillion budget has a recurrent expenditure of approximately N8.2 trillion and a capital expenditure of N5.9 trillion, while debt servicing increased from N6.31 trillion to N6.6 trillion.

Economists say the rise in debt servicing and massive borrowings to fund fuel subsidy have negative effects on the economy, especially the real sector.

This, in turn, has massive implications for the cost of funds for businesses and the private sector.

The Chief Executive Officer of Cowry Assets Management Limited, Johnson Chukwu, posited that if the government did not exercise caution on borrowing to fund its budget deficit, the private sector would be suffocated by the cost of funds for business.

Chukwu said, “When we talk of the budget deficit of N12 trillion today, we are also talking of a national debt of more than N22 trillion. If the Federal government continues to borrow, the implication is that you are going to crowd out private sector funding for the real sector.

“The increase in projected revenue only gives incentives to spend more even when we haven’t met up with it in the last five years. Now, this has made us to increase the budget deficit, which is putting lots of pressure on our funding the private sector.”

The economist warned that Nigeria may head the way of Ghana if it failed to address its appetite on “unregulated borrowing.”

The Debt Management Office (DMO) spoke in a similar vein during a budget presentation to the federal legislators, stressing that massive borrowing to fund the budget could see the Buhari administration leave a whopping N77 trillion for the incoming administration.

Experts’ concern on overburdening tax in 2023

The Nigeria Employers’ Consultative Association (NECA) has expressed worry over the number of taxes imposed on businesses in the country.

According to the Director-General of NECA, Adewale-Smatt Oyerinde, organised businesses are burdened by over 50 different taxes, levies and fees, both legally and illegally.

Smart-Oyerinde frowned at some of the provisions of the Finance Bill 2022 recently passed by the National Assembly, particularly the increase in Tertiary Education Tax (TET), from 2.5 cent to 30 per cent, saying it was increased without regard for the economic woes businesses are facing.

“Taxes being paid by businesses in Nigeria include company income tax, stamp duties, petroleum profit tax, capital gains tax, value added tax, personal income tax, withholding tax and tertiary education tax. Increasing the Tertiary Education Tax is another burden too much.

“Also, increasing the Company Income Tax rate for a gas-flaring company from the standard 30 per cent to 50 per cent is also worrisome, considering the fact these companies are already covered in the Petroleum Industry Act. This can be a recipe for further divestment.

“Also, imposition of excise duty at rates to be specified via presidential order on all services, including telecommunication services, is too broad and vague. This can be subjected to abuse and further strangulation of the business community,” he said.

He urged President Buhari to request the National Assembly to take into cognisance the concerns of organised businesses. He also mentioned the need to expunge all anti-business provisions in the bill.

The Director-General of the Budget Office of the Federation, Ben Akabueze, also identified taxes as a hedge to inflation, although he did not see the Nigeria context as that terrible.

Akabueze said, “It is not right to overburden investors with taxation. However, the situation is not as dire as it seems. In Germany, corporate tax is 29.8 per cent. When we compare ours with the global standards, we would be surprised that 30 per cent on corporate tax is not that high.”

Experts suggestions, way forward in 2023

To unlock growth and investment in 2023, the government must undertake some urgent reforms, analysts say.

Yusuf, describing the enactment of the Petroleum Industry Act as a major step towards the reform of the oil gas sector, said the government, however, needs to demonstrate greater commitment to its implementation.

“The deregulation of the petroleum downstream sector is a major economic reform imperative. This is inevitable if we must unlock investment in the sector and put an end to the perennial fuel scarcity and the monopolistic structure of the sector,” he said.

On power reforms, he called for an enabling environment that would enable the private sector to drive results.

“An enabling environment must be created to sustain current private sector investment in the sector and attract new private capital to the electricity sector. Urgent reforms are vital with respect to electricity tariff, metering and deepening of energy mix. We need robust incentives (fiscal and monetary) to boost private investment in renewable energy.

“We should reform the budget and appropriation processes to prioritise infrastructure financing and human capital development. This would boost productivity and competitiveness of the economy,” he added.

Adoption of these reform initiatives, Yusuf was positive, would guarantee progression towards fiscal consolidation and reduction in fiscal deficit, while diminishing the need for borrowing and abating the debt service burden.

The consensus is that Buhari has not, in his seven and a half years as president, exhibited the will, if not competence, to tackle economic turbulence. Under his watch, the economy has been taking a tumble rather than stability. So, would he be able to bring some progress to the economy in only five months,? The time ticks.

Harrison Edeh is a journalist with the International Centre for Investigative Reporting, always determined to drive advocacy for good governance through holding public officials and businesses accountable.