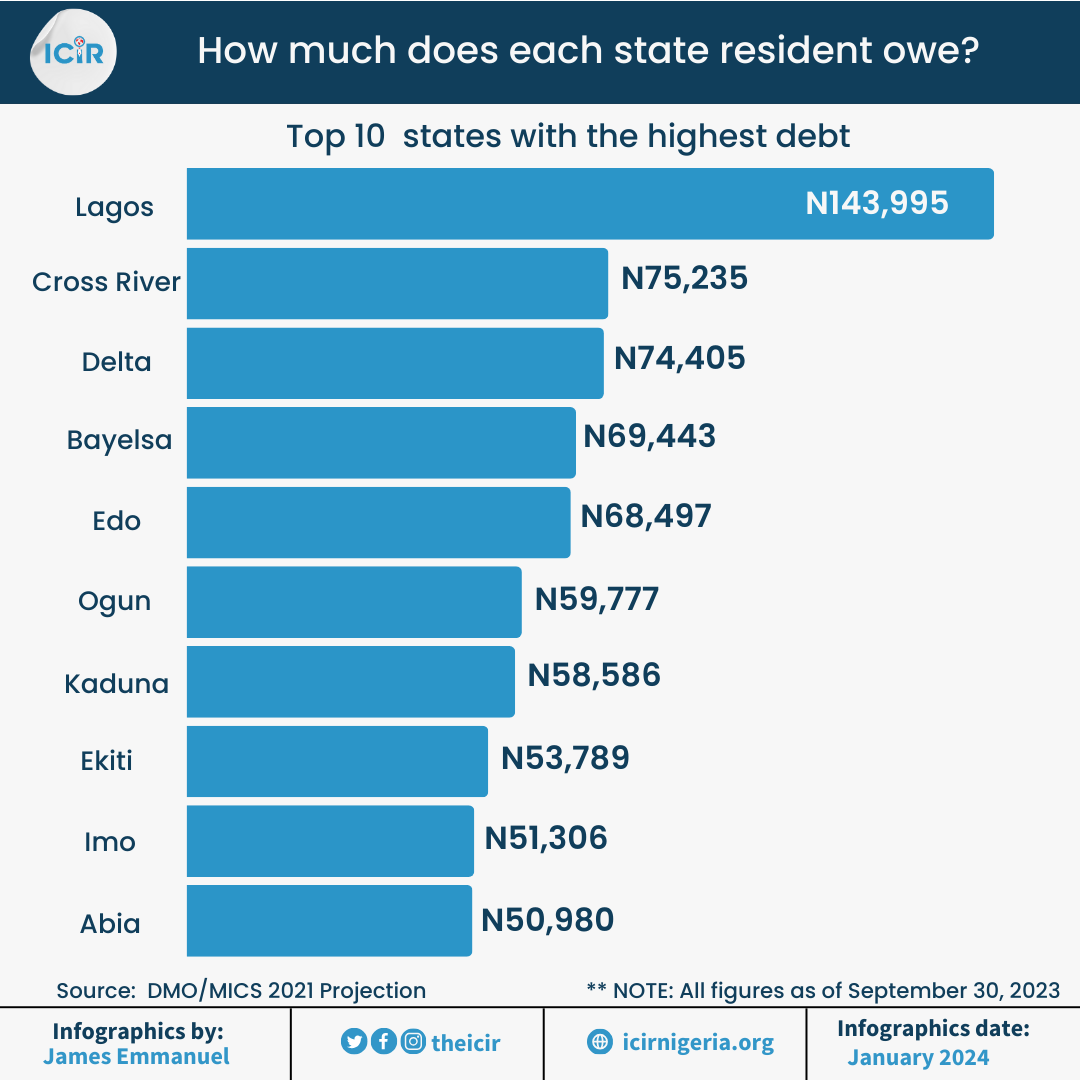

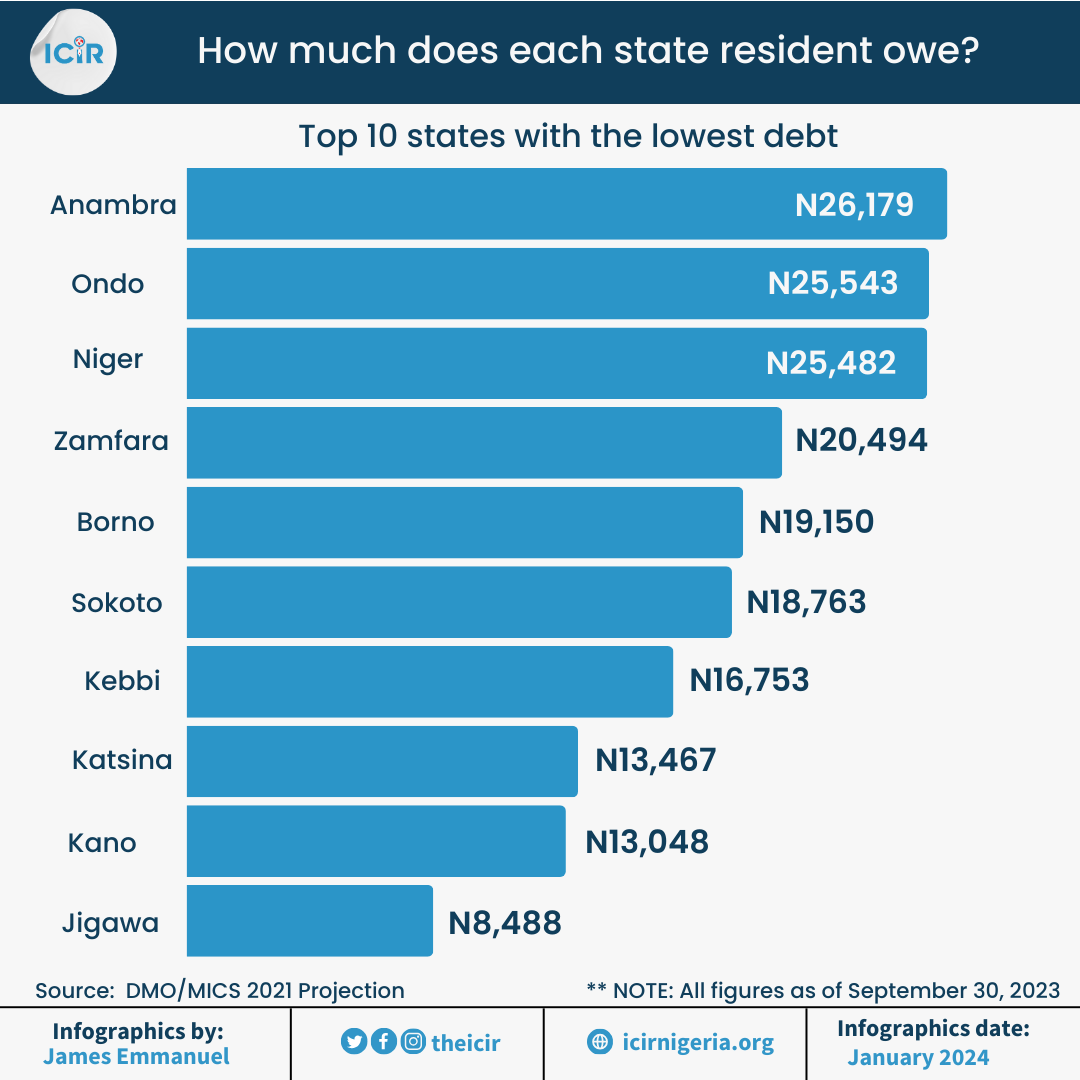

FOR every N8,488 owed by a resident in Jigawa state, another resident living in Lagos State owes about 17 times more, an analysis by The ICIR has shown.

The ICIR analysed the public debt stock, juxtaposing it with the projected population of each state, using data released by the National Bureau of Statistics (NBS).

While public debt is calculated by adding a nation’s domestic and external debts together, debt per capita is calculated as the total public debt of a country divided by the country’s population.

According to NBS, as of the third quarter of 2023, Lagos, with a population of 13.4 million, had a total public debt of N1.93 trillion, while Jigawa, with a population of 7.4 million, had a debt stock of N63.14 billion.

By calculation, this means that each resident living in Lagos state owes N143,995 in debt per capita, while Jigawa state residents owe N8,488 each.

The NBS data show that as of the third quarter of 2023, Nigeria’s public debt stock stood at N87.91 trillion ($114.35 billion). When broken down, the total external debt was N31.98 trillion ($41.59 billion), while the total domestic debt was N55.93 trillion ($72.76 billion).

Interpreting the figures in percentages, 36.38 per cent of the total debt stock is external debt, while the domestic debt is 63.62 per cent.

As of the second quarter of 2023, The ICIR reported how each Nigerian owed N396,376.19 in terms of debt per capita when the country’s public debt stock was N87.38 trillion ($ 113.42 billion).

If the country’s debt per capita is calculated as of the third quarter of 2023 with a projected population figure of 216,783,381, each Nigerian will owe N405,520.

This is a growth of N9,143.81 in the space of three months.

State’s debt analysis

Data by NBS showed that the total domestic debt for the 36 states and FCT was N5.74 trillion, while the external debt stood at N3.35 trillion ($4.35 billion).

This brings the total public debt of the states to N9.09 trillion.

If states’ debts are calculated within the period, the states with the highest debt are Lagos state with N1.93 trillion, Kaduna state with N525.58 billion, Delta state with N417.38 billion and Ogun state with N379.26 billion.

Meanwhile, the states with the lowest debts are Jigawa, Kebbi and Taraba, with N63.14 billion, N92.40 billion and N99.01 billion, respectively.

Based on this analysis, residents living in Lagos State would pay almost 17 times more than those in Jigawa State.

Revenue and debt

To secure funding, a state could either generate internal revenue (IGR), rely on the Federal Government’s monthly allocation (FAAC) or borrow money internally and externally (public debt). To repay the debt would mean the state must increase internally generated revenue.

For instance, Lagos State has a population of more than 13 million residents, making it the second most populated state in Nigeria, compared to Jigawa, with a population of 7.4 million.

Despite the wide gap between the two states in population and debt stock, there is also a wider margin in revenue generation.

As of 2022, Lagos state had a total revenue of N812.07 billion, of which 80 per cent was generated internally. If channelled into paying off debt, this amount could drop the current debt figures by 58 per cent.

Meanwhile, Jigawa state, with total revenue of N91.10 billion as of 2022, depended on the Federal Government’s intervention for 77 per cent of its revenue. If this is channelled into debt repayment, only 44 per cent of the debt will be cleared off.

Additional findings showed that Kano state, the most populated state in Nigeria with more than 15 million people, had a debt per capita of N13,048. It is the second-lowest debt per capita for the third quarter of 2023.

Also, Bayelsa state, which has the lowest population in Nigeria, was ranked among the first four states with high debt per capita. This is N69,443 for each of the 2.5 million residents in the state.

A senior research & policy analyst for BudgIT, Vahyala Kwaga, told The ICIR that between 2018 and 2022, the 36 states and FCT total debt grew by 45.89 per cent. With the recent policies across the exchange rate devaluation, there are possibilities that the debts would increase.

He said, “It must be mentioned that debt is not bad, per se. Where debt is acquired for demonstrably revenue-generating projects, one can support such borrowing. But where loans are taken to pay salaries, overheads, or white elephant projects that are the pet projects of governors, such should be discouraged.”

He added that states with high debt burdens should borrow only for developmental projects, while governors should cut down the cost of governance by plugging leakages and ensuring tax and non-tax revenue administration.

[The sheet used for this analysis can be accessed here and here]

Kehinde Ogunyale tells stories by using data to hold power into account. You can send him a mail at jameskennyogunyale@gmail or Twitter: Prof_KennyJames | LinkedIn: Kehinde Ogunyale